French Banking Industry

Press conference: address by the President of the FBF

Address by Daniel Baal, President of the French Banking Federation

Good morning everyone,

First of all, I would like to thank you for being here today at the French Banking Federation to discuss the key issues shaping the start of this year. I extend my best wishes to you, to your loved ones and to your organisations. I also wish the very best for France, its economy and the French people.

At the beginning of this year, I would like to give you an overview of our actions and concerns across several areas.

In a few moments, I will hand over to Frédéric Dabi, who will present the results of the IFOP survey. Let me highlight straight away one key finding: nine out of ten French people have a positive image of their bank.

I will endeavour to be as concrete as possible. Some “banking” issues may appear complex or technical—particularly when it comes to regulation—but make no mistake: they have a direct impact on the daily lives of French people and on business activity. These issues are sometimes overlooked, misunderstood or even caricatured. Our role is to bring clarity, as I have recently done regarding the Livret A savings account and overdraft facilities.

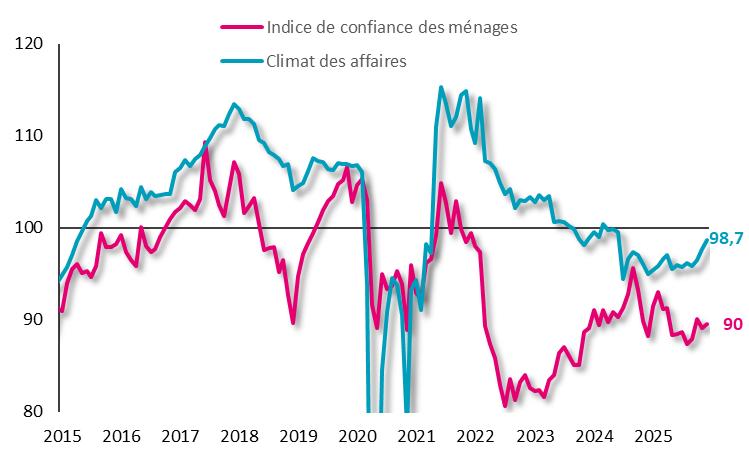

Despite an exceptionally high level of uncertainty, 2025 demonstrated the resilience of both the banking sector and the French economy. Economic, geopolitical, domestic political, budgetary and fiscal uncertainties have accumulated. Taken together, they weigh on the confidence of households and businesses (1) and delay private and public investment projects across France.

Against this backdrop, two certainties stand out. The first is what Mark Carney aptly described in Davos last week as “the breakdown of the world order, the end of a comforting fiction and the beginning of a brutal reality in which the geopolitics of major powers are no longer constrained.” The second is the imperative for a France that is fully mobilised within a strong, united and effective Europe.

In this context, my first message is clear: French banks have fully played their role—solidly, responsibly and consistently.

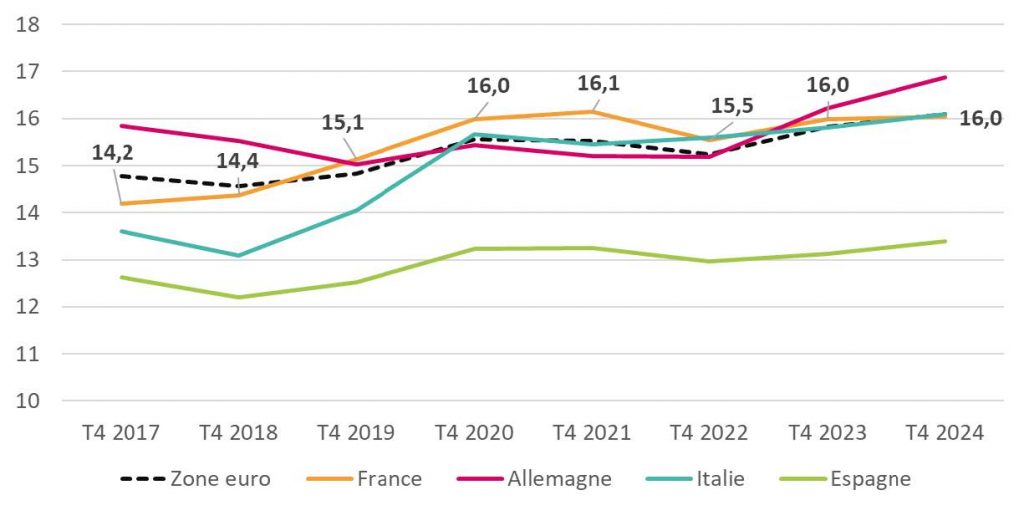

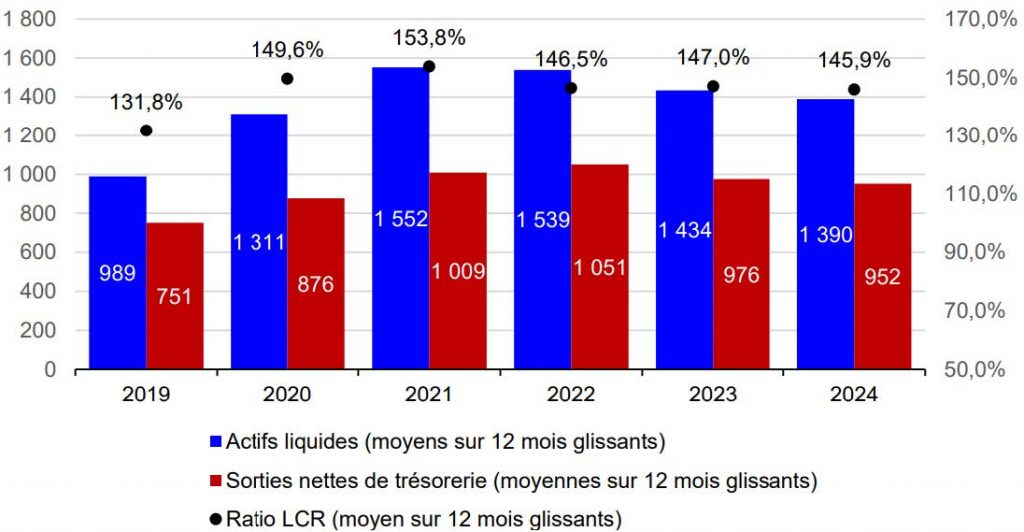

Solidly, first and foremost. Today, our institutions rank among the safest in the world. Their intrinsic quality is excellent, capital levels are high and liquidity is abundant. This has been confirmed by European stress tests (2).

However, solidity is not an end in itself. It is there to serve the real economy. French banks support it everywhere and for everyone, with a strong sense of responsibility.

In 2025, French banks continued to finance businesses, even at a time when caution could have prevailed. Business failures are at a historic high—it is true. But risk is our business. The entire profession is mobilised to support business leaders and their employees.

Banks have supported a remarkably dynamic entrepreneurial fabric, which may have scaled back investment but was able, thanks to the banking sector’s support, to find positive financing solutions. In total, more than €1,400 billion in loans to businesses are outstanding in France—an increase of 62% over ten years. In 2025, nearly €30 billion per month financed businesses of all sizes. That is €1 billion per day invested in the future of our country. By contrast, French public debt is increasing by around €500 million per day. Banks are choosing the future; the State, too often, is choosing inertia.

We have also supported the gradual recovery in mortgage lending and, through it, the entire housing sector. Outstanding housing loans to households in France stand at €1,283 billion, with a recovery trend in 2025, notably thanks to declining interest rates. The average interest rate, around 3%, is among the lowest in Europe. Fixed-rate loans—a French specificity—provide strong protection for both existing and new borrowers.

Moreover, first-time buyers account for more than 50% of mortgage lending for primary residences in 2025, as do lower-income households. This clearly demonstrates the essential role played by the banking sector in enabling access to home ownership for as many people as possible.

French banks have never shut off mortgage lending. In our model, supporting home ownership is fundamental. At a time when housing is one of the main concerns of our fellow citizens—and of banks as well—the strong market recovery is good news for everyone.

My second message is to recall what makes all this possible: French banks are largely built on a universal, relationship-based, proximity-focused model that supports projects over the long term.

Let me recall a few concrete indicators of this proximity:

- Nearly one in three bank branches in the euro area is located in France.

- More than 99.9% of French citizens have access to cash within fifteen minutes of their home.

- This is made possible thanks to the commitment of over 370,000 women and men across the country who deliver this universal banking service every day.

There may be prejudices, clichés or questions about banks. We are used to this and we systematically engage in dialogue to explain and to find solutions whenever possible—as we once again demonstrated during the Covid period.

Today, banks are clearly part of the solution to the difficulties faced by households, businesses and even the State. That is my third message. This solution-driven mindset guides us every day, both within banks and within the French Banking Federation. The IFOP survey results that Frédéric Dabi will present shortly both confirm this and reinforce our responsibility.

During the crises that followed the Covid period—energy, inflationary and geopolitical—banks once again rose to the challenge. I say it forcefully: French banks are a valuable asset for France and for Europe.

The defence sector provides a clear illustration. French banks have long supported the French and European defence industries. As of 30 June 2025, and announced here for the first time, the six largest French banking groups—BNP Paribas, BPCE, Crédit Agricole, Crédit Mutuel, La Banque Postale and Société Générale—had provided €45 billion in financing to French defence companies. This represents a 75% increase since 2021 and already +22% in the first half of the year. An additional €22 billion has been granted to other European defence companies. These figures highlight the capacity of French banks to support defence efforts in a geopolitical context marked by rising tensions and conflicts, and by the need for a European response.

Another key priority for us is financing the energy transition. Banks are acutely aware that the climate emergency is the defining challenge of our generation. According to experts, France could face a temperature increase of +2.7°C by 2050—and 2050 is tomorrow in our business. If you need convincing of our commitment, consider this: will the 25-year mortgages we grant today be repaid if the homes they finance become uninhabitable?

French banks are continuing to redirect financial flows towards their customers’ transition projects—whether businesses, local authorities or individuals. As every year, the FBF published its benchmark study in April 2025. Let me recall its key findings:

- With €96 billion in renewable energy financing, French banks are global leaders (+28% between 2023 and 2024).

- Green and sustainable loans on their balance sheets rose by 27% in one year, from €372 billion in 2023 to €471 billion in 2024.

- At the same time, French banks’ exposure to the hydrocarbon sector fell by 15% in 2024, to €37 billion (0.36% of total assets).

- Today, for every €1 financing fossil fuel production, €2.6 finance renewable energy, and more than €12 finance green and sustainable loans.

The strategy remains unchanged: banks will continue their long-term efforts to support the economy and their customers in decarbonising their activities. Data as at end-2025 will be published later this year.

Looking ahead to 2026, financing needs continue to grow to address energy, technological and societal transitions, as well as the major challenge of European sovereignty. Power dynamics are shifting faster and more forcefully at Europe’s borders and beyond. Collective action is urgently needed—and French banks are fully playing their part. Our responsibility also requires us to speak out when collective choices threaten our ability to act or have tangible consequences for citizens’ daily lives.

France’s public finances are a source of concern, and the latest version of the draft Finance Bill raises more questions than it answers. Over recent months, all economic actors have witnessed escalating tax pressure, which cannot constitute a sustainable response to our country’s economic and social challenges. In 2024, French banks contributed more than €22.3 billion to public finances—up on 2023. This exceeds the combined budgets of the ministries of sport, Europe and justice for 2026, which amount to €20.5 billion.

Fiscal decisions are not neutral for future growth. In this regard, I have been struck by the controversy surrounding business support. Some claim that large French companies enjoy privileges. In reality, they are burdened by heavier taxation than their European peers. Factually, net business taxation exceeds that of our neighbours: 10.5% of GDP, compared with 8.1% for the EU average and around 7% in Germany (FIPECO).

Taxing “Made in France” through the renewal of the corporate surtax penalises responsible actors who locate jobs and income in France and ultimately weakens our economic sovereignty. It also undermines commitments previously made and generates instability for businesses. With a corporate tax rate of 36.13% for large companies subject to the surtax (KPMG/OECD), France stands well above the OECD average of 24.1%.

Overtaxing businesses risks negative consequences—for growth, investment, purchasing power and employment, and ultimately for tax revenues themselves.

Banks, like all companies, are now among the few places in society where strong cohesion exists around a shared project. Business leaders and employees alike aim to create more value in order to share it internally and externally—with society and with the State. Businesses are a cornerstone of stability and cohesion, and the French people understand this well.

Let me now turn briefly to savings. We sometimes hear talk of “money lying idle” in accounts and savings products, or claims that lower savings rates are bad news for savers, or that banks are not doing enough to promote the Livret d’épargne populaire (LEP). These debates highlight the importance of financial education, which we actively promote through initiatives such as Les clés de la banque and Invite a banker into my classroom, in which I will personally take part this year.

- No, money does not lie idle in banks. Deposits and savings fuel the real economy. They enable banks—and the Caisse des Dépôts for its share—to lend to households, businesses, local authorities, social housing and infrastructure. Savings are not unproductive, contrary to what some MPs have sought to suggest.

- As for the Livret A, let us dispel the monetary illusion. With inflation at 0.8% in France, a nominal rate of 1.5% offers a positive real return. The Livret A remains a highly attractive product: zero risk, tax-free, fully liquid and with a high ceiling. For long-term projects, savers can then turn to other products such as life insurance, retirement savings plans (PER), equity savings plans (PEA) or term accounts. France benefits from a comprehensive and competitive savings ecosystem that serves savers of all profiles.

- LEP accounts increased from 6.9 million holders in 2021 to over 12 million in 2025—a rise of more than 75%. This would not have been possible without banks’ active promotion. We work closely with the authorities on outreach campaigns, and I echo the call made by the Minister of the Economy on 15 January encouraging eligible citizens to contact their bank to open such accounts.

I will conclude the national section by addressing payment fraud. Payment security is an absolute priority for French banks.

We invest continuously. Let me give three concrete examples visible to customers every day:

- Strong customer authentication using at least two independent factors.

- Redesigned app interfaces to clearly display transaction details and allow customers to approve or reject payments.

- Since 9 October 2025, the Verification of Payee (VoP) service, which secures transfers by checking that the beneficiary name matches the IBAN.

The fight against fraud is a shared responsibility, including on the part of customers. I would stress that it is essential for customers to remain vigilant at all times, and not only when making payments.

To raise awareness, the banking sector mobilises hundreds of millions of euros every year—through educational initiatives, dedicated teams, artificial intelligence and other tools. In the media, banks and the French Banking Federation launched a large-scale awareness campaign in 2023 entitled “Don’t share these details”. We relaunched this campaign in 2024 and 2025, this time in close coordination with public authorities and regulators, in addition to each bank’s own customer information initiatives. We will be launching a new campaign again in 2026.

Lastly, we firmly believe that combating fraud can only be truly effective if all stakeholders are involved.

- The law of 7 November 2025 on payment fraud provides a clear illustration of this approach. The banking profession initiated this project several years ago, and it will now be made operational thanks to the legislative framework proposed by Daniel Labaronne. From early May, it will enable the rollout of an information-sharing tool on payment accounts suspected of being used for fraudulent purposes. Fraudsters will no longer be able to act more than once using the same account.

- It is also essential that the obligations set out in the 2021 law to block fraudulent calls are fully implemented, which is the responsibility of telecom operators. Since 1 October 2024, certain calls that are not authenticated by operators must be cut off. These initial measures should have an impact on spoofing fraud—a scam technique whereby fraudsters impersonate a bank advisor by phone—but they must be extended to cover all fraudulent calls and text messages, and rolled out at European level.

- Today, however, my most solemn appeal is addressed to social media platforms and email service providers. They must play an operational role in preventing, deterring and combating fraud and scams, particularly investment scams. This is a call to public authorities and regulators, in France and in Europe, to take action. Recent studies and media investigations shed light on the scale of the issue. According to the UK regulator, in 2023, “more than half of scams involved Meta platforms (Facebook, Instagram, WhatsApp)”. According to documents obtained by Reuters, Meta estimates that 10% of its total revenue for 2024—around USD 16 billion out of more than USD 160 billion—came from advertising promoting scams, fraudulent investment schemes and similar activities. Meta is estimated to broadcast around 15 billion fraudulent advertisements every year. These figures demonstrate the massive scale of scam dissemination and the lack of effective action to address it.

We will continue to mobilise tirelessly to further strengthen the security and information provided to our customers. However, if we genuinely want to protect French and European citizens, Europe must address the issue of platforms’ inaction in the face of scams disseminated through their services. We hope to be heard on these two key issues: prevention and cooperation. As the IFOP survey will show, while 73% of French respondents say they trust banks to secure their personal data, only 41% say the same of Big Tech companies.

The issue of fraud provides a natural transition to the European challenge: do we have the means to finance our future, and is Europe giving itself every opportunity to do so? The ecological transition, reindustrialisation, innovation, defence, housing and digital sovereignty all entail immense financing needs.

Yet today, billions of euros in capital are immobilised by an accumulation of prudential constraints that are sometimes disconnected from economic realities. Additional requirements imposed by supervisors between 2021 and 2024, based on a sample of fifteen banks, are estimated at more than €100 billion. This represents a financing potential of around €1.5 trillion effectively blocked for Europe. Several initiatives currently under discussion at European level risk further limiting bank financing of the economy. I will mention just three examples, among many others:

- Housing: we are facing requirements that are increasingly disconnected from the real economy and that undermine France’s effective mortgage lending model. For example, there are proposals to require third-party valuation of mortgaged properties in France. This would increase costs, lengthen processing times and diminish the role of notaries. Moreover, the full implementation in Europe of the Basel agreements concluded in 2017—reflecting a very different context—would only be postponed by a few years for housing, while the United Kingdom, Canada and the United States are stabilising, easing or not applying these constraints. All this makes mortgage lending increasingly complex and ultimately penalises our fixed-rate system in favour of variable rates, which are far less protective for households. It bears repeating: French banks, through their fixed-rate lending model, played a crucial shock-absorbing role during an inflationary shock unprecedented for households in the past 40 years. Elsewhere, variable rates dealt a severe blow to household budgets. Our model must be defended.

- Regulation: Europe is at a crossroads and must make clear choices to remain in control of its own destiny. The Trump administration has launched a broad deregulatory drive—for example, we have yet to see the US proposal for the final implementation of Basel III, even though it has been in force in Europe for over a year. We are not calling for such deregulation, which would be unhealthy. However, unnecessary obstacles to financing the European economy must be identified and removed. Studies consistently show that bureaucracy—emanating from Brussels, but also from France—harms our economy. It costs around €100 billion per year (IFRAP, 2022). Elsewhere, systems are simplified, innovation is encouraged and factories are built; here, we innovate in complexity or create regulatory labyrinths. My concern is that Europe will repeat the same mistakes tomorrow.

- Payments: the central bank digital currency (CBDC) project continues to move forward. Unlike all other central banks outside China, the European Central Bank is pushing ahead rapidly with a retail digital euro. The European Commission and the European Council expressed their support in December 2025, even though questions remain. The European Parliament is now examining the issue.

- This retail digital euro project—which, at best, could not be implemented before 2029—is a strategic and political mistake. It will not resolve the issue of European sovereignty in payments, nor will it establish the euro as an international currency.

- If it is nevertheless pursued, we are making proposals to make the project less harmful, particularly by relying on existing infrastructures—such as instant payments, which work very well—requiring the use of European solutions and limiting holdings of digital euros.

- We are also hearing calls for a public-private partnership on the retail digital euro. In principle, we share the willingness to work together on this issue, as on others. Currency has always been based on a public-private balance. Digitalisation should extend this balance, not undermine it. That said, a partnership is only meaningful if each party has a clear role and if the general interest is served without weakening the financing of the economy.

- If the goal is to create a “European Airbus of payments”, we must first build on infrastructures and use cases that already exist but need to be scaled up—such as instant payments and Wero. Creating a new form of currency would risk unnecessarily competing with European solutions currently being rolled out and could even slow down the implementation of an effective solution.

- Affirming European sovereignty in the constrained environment we face means focusing our efforts on tools that already work well today. Private solutions—supervised and regulated by European authorities—demonstrate this clearly.

Beyond the retail digital euro, however, the real technological and sovereignty challenges for Europe lie elsewhere: the wholesale digital euro, tokenised deposits and euro-denominated stablecoins. These are now major issues. If we want to offer a credible alternative to the US dollar, this is the direction we must take.

Furthermore, the European financial sector as a whole—including insurers—has sounded the alarm on the proposed regulation on access to financial data (FiDA), a text that is dangerous both for sovereignty and for risk mutualisation. We reiterate that this proposal must be abandoned.

On all these issues, we call for a better balance in favour of the European economy—between stability and competitiveness, between regulation and growth. We also want European sovereignty to be translated into concrete action, beyond words, with genuine support for the European model and the economic actors that serve it.

Europe, as a community based on the rule of law and justice, must serve individuals and human, social and economic progress. It must articulate a clear vision, faithful to that of its founding fathers, and stop constantly introducing new, unnecessary—or even costly and ineffective—regulations, such as FiDA and the retail digital euro.

In conclusion:

At a time of international, European and national uncertainty, the French banking sector is both a factor and an actor of stability, cohesion and long-term vision. It is solid, committed and deeply rooted in local communities. The French people recognise this clearly: 83% say that the banking sector is strategic.

The sector continues to play its full role in financing the ecological transition, innovation, sovereignty at all levels and societal challenges. To meet these challenges, it needs a clear, stable framework that ensures a level playing field.

There is a path between deregulation on the one hand and over-regulation on the other. My message is simple: without strong, innovative and competitive European banks, there will be neither European sovereignty nor successful transitions.

Success will only come through collective effort—public authorities, businesses, individuals and social partners alike. Let us engage in dialogue. Let us not pit stakeholders against one another. And let us place our trust in those who invest, support and build for the long term.

Thank you for your attention. I now hand over to Frédéric Dabi to present the main findings of the IFOP–FBF survey. Frédéric Dabi, Maya Atig—our Chief Executive Officer—and I will then be available to answer your questions.

Annexes

(1) Household confidence and business sentiment in France – source: INSEE

(2) Comparison of the Common Equity Tier 1 (CET1) capital ratio of European banking groups – source: ECB

Short-term liquidity ratio of the main French banks – source: ACPR

Address by the President of French Banking Federation – 26 january 2026 (PDF)

444.59 Ko

0 document bookmarked